Structured Generational Wealth Creation

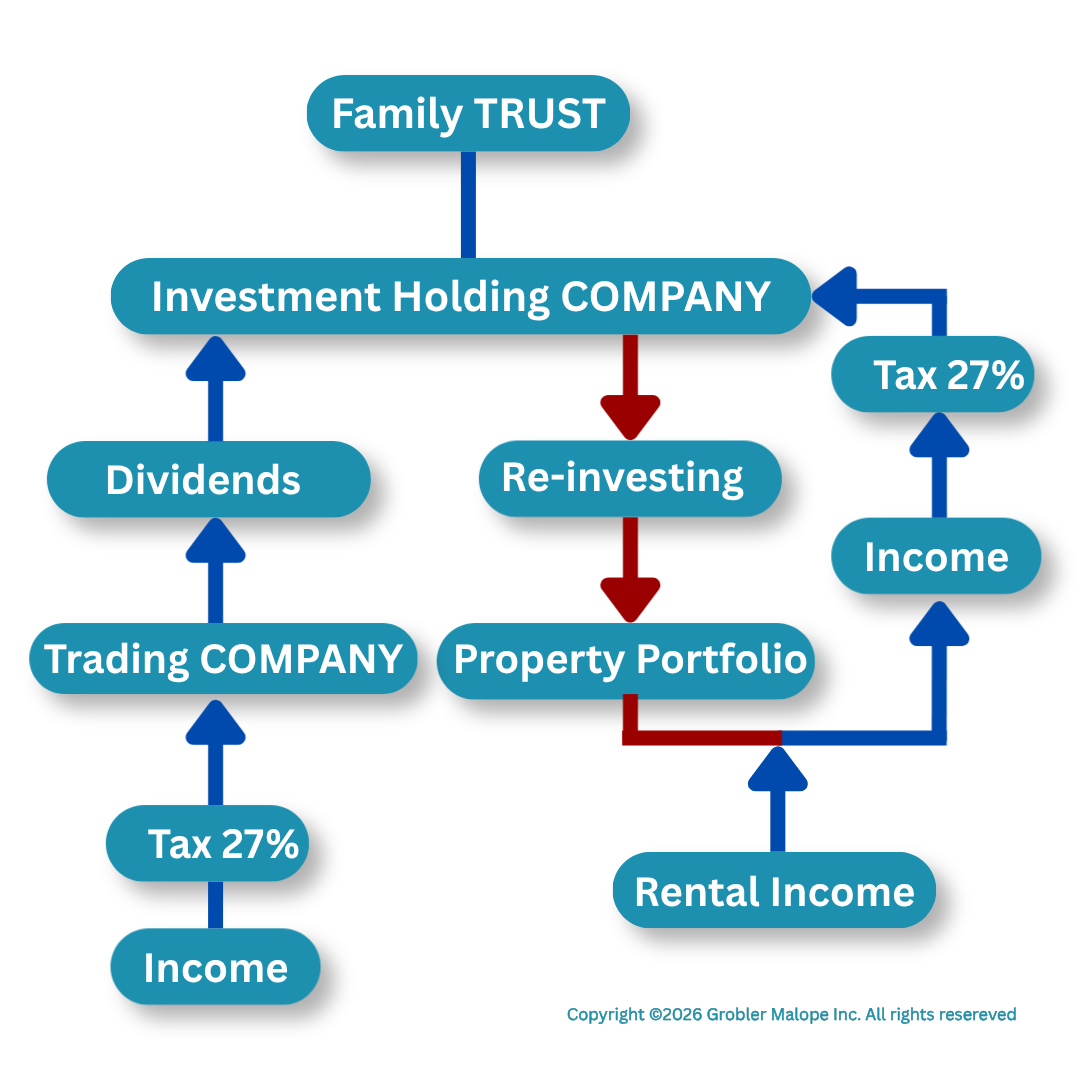

The diagram illustrates a structure used by Grobler Malope Incorporated for clients as a South African asset protection, estate planning and wealth creation structure, consisting of three separate entities:

- A Family Trust

- An Investment Holding Company

- A Trading Company

Each entity serves a different purpose and is intended to separate wealth accumulation from business risk.

The Structure Explained

The process starts with the establishment of a Family Trust. The Family Trust becomes the shareholder of a private company that serves as the Investment Holding Company. Although you may act as a director of the Investment Holding Company and control its day-to-day affairs, the shares are owned by the Trust and not by you personally. The Investment Holding Company then becomes the owner of investment properties, long-term investments, share portfolios, vehicles and equipment used as investments, and other wealth-generating assets. The properties owned by this company collectively form its Property Portfolio. A key objective of this structure is that the assets are legally owned by the company whose shares are owned by the Trust, rather than by you in your personal capacity. Provided the structure is properly implemented and administered, this creates a degree of separation between your personal estate and the assets accumulated within the structure.

The Basic Flow Explained

Step 1 – Business Operations

A separate Trading Company is registered through which all business activities are conducted. This company renders services, and or sells products, employs staff, incurs operational expenses, and assumes normal commercial risks. All trading income is earned by this company.

Income → Tax → Profit

Income generated through business activities flows into the Trading Company. The company then pays salaries, suppliers, operating expenses, overhead costs, and SARS. Company profits were subject to 27% corporate income tax at the time this diagram was created. After expenses and tax, the remaining profits may be declared as dividends. Provided that structure is done and operated correctly, if business operation ever fail, the Trading Company can be liquidated and wound-up without any risk to the Investment Holding Company and its assets.

Step 2 – Dividends Flow to the Investment Holding Company

The Trading Company pays dividends to the Investment Holding Company. Because the shareholder is another South African resident company, these dividends are generally exempt from dividends tax in terms of the Income Tax Act. This allows profits to move from the Trading Company into the Investment Holding Company without the immediate leakage normally associated with dividends tax. The result is that business profits can be extracted from the operational company and accumulated in a safer, asset-holding environment.

Step 3 – Building the Property Portfolio

The Investment Holding Company uses these profits to purchase commercial and residential properties, acquire long-term investments, invest in listed shares, and purchase income-producing assets. These assets form the company's growing Property Portfolio. Rather than distributing profits for personal consumption, the focus is on acquiring assets that generate additional income.

Step 4 – Rental Income and Investment Returns

As the property portfolio grows, rental income begins flowing back into the structure. The Property Portfolio generates rental income, capital appreciation, investment returns, interest and other passive income. After allowable deductions and expenses, the net income is taxed at the applicable company tax rate. The remaining profits then flow back into the Investment Holding Company.

Step 5 – Re-Investing

Instead of distributing profits to individuals, the Investment Holding Company re-invests those profits into additional properties and investments, new opportunities, and debt reduction on existing assets. A continuous wealth generating cycle is generated, and over time, the structure creates an expanding pool of income-producing assets.

Why Separate the Trading Company and the Assets?

One of the most important reasons for using this structure is risk segregation. The Trading Company is exposed to lawsuits, creditors, business failures, contractual disputes, employee claims, and commercial risks. The Investment Holding Company owns the valuable assets. This means the assets are not directly held by the business that faces daily operational risk. The most successful entrepreneurs follow the principle:

"Trade in one company. Hold wealth in another."

This ensures that assets accumulated over many years are not unnecessarily exposed to operational business risks.

Estate Planning Advantages

The Family Trust adds an additional layer of succession planning, because the Trust can:

- Continue after your death;

- Hold shares for future generations;

- Prevent fragmentation of assets by provide continuity and stability.

- Avoid repeated transfer costs on succession.

Instead of transferring multiple properties and investments upon death, control of the Trust can continue according to the Trust Deed.

Important Considerations

Although this structure can be highly effective, it is not a "magic shield". Courts can disregard structures that are used for fraud, improperly administered, or to evade creditors as opposed to protect against creditors. The Trust and companies must operate as genuine, separate legal entities. It should be noted that SARS anti-avoidance rules apply - South Africa has extensive Trust taxation provisions, anti-avoidance measures, attribution rules, and capital gains tax provisions. It is important that professional tax advice be obtained before implementation. Professional administration is essential, and the structure should have:

- Proper Trust and company resolutions;

- Separate bank accounts;

- Independent accounting records, and annual financial statements;

- Tax compliance.

Failure to maintain proper governance can undermine the benefits of the structure.

In Summary

The diagram illustrates a wealth-building cycle allowing business profits to be converted into long-term assets, creating a growing portfolio of investments and income-producing properties while simultaneously separating operational business risk from accumulated wealth.

Asset protection, taxation, trust administration and succession planning should always be structured with advice from an attorney, accountant and tax practitioner familiar with South African law and SARS requirements.

Copyright © 2026 Rohan Lamprecht. Disclaimer: The information in this article is of a general nature for educational purposes only, relevant to the publishing date. Any opinions expressed are solely those of the author and do not necessarily reflect the views or opinions of Grobler Malope Inc. The content is not intended to constitute professional or legal advice, and you are encouraged to call and consult with our attorneys to discuss your specific situation before making any decisions. Grobler Malope Inc - 087 057 1790 - info@gmilaw.co.za